The Best Home Loan Options for First-Time Buyers

One of life’s greatest achievements is purchasing your first house, but it can also be one of the scariest. Between learning new terminology, saving for a down payment, and understanding the various loan options, many first-time buyers feel overwhelmed before they even begin. The truth is, finding the right home loan doesn’t have to be complicated. With the right knowledge and preparation, you can align your financial goals with the loan that best fits your lifestyle and long-term plans.

This guide breaks down the best home loan options designed for first-time buyers, so you can make an informed, confident decision about financing your new home.

Understanding How Home Loans Work Before You Dive In

Buying a home isn’t just about choosing the right property—it’s about understanding the financial foundation that makes homeownership possible—for first-time buyers, grasping the basics of how home loans work can prevent future stress and help you spot a good deal when you see one.

Buying a home isn’t just about choosing the right property—it’s about understanding the financial foundation that makes homeownership possible—for first-time buyers, grasping the basics of how home loans work can prevent future stress and help you spot a good deal when you see one.

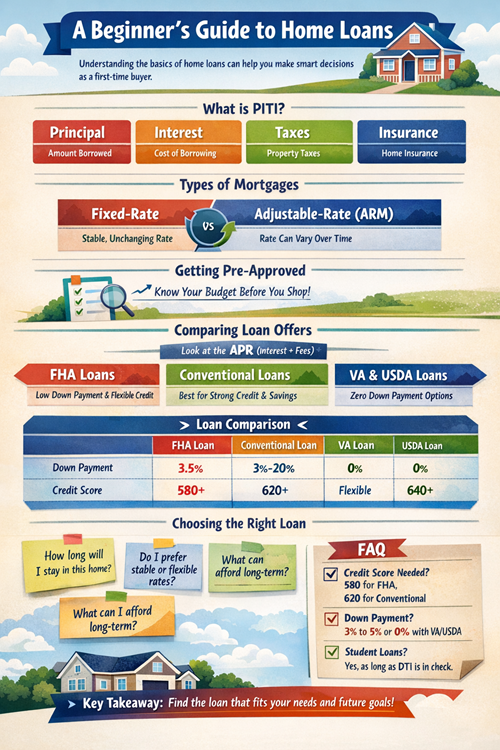

A home loan (mortgage) is a long-term agreement where a lender provides funds for you to purchase a home, and you agree to repay that money—plus interest—over time. The majority of home loans have terms between 15 and 30 years, and each monthly payment usually consists of four essential elements, commonly known as PITI:

- Principal: The amount of money borrowed to buy the home.

- Interest: The cost of borrowing that money, expressed as a percentage.

- Taxes: Your local government collects property taxes.

- Insurance: Homeowners insurance that protects against damage or loss.

There are two main types of mortgages:

- For fixed-rate mortgages, the interest rate doesn’t change during the course of the loan. For purchasers who like consistency and intend to live in their house for a long time, these are perfect.

- Adjustable-rate mortgages (ARMs), whose rates can change after an initial period. ARMs often start with a lower rate, which makes them appealing for buyers planning to sell or refinance within a few years.

Before you even start house hunting, it’s smart to get pre-approved for a loan. Pre-approval isn’t just a rough estimate—it’s a detailed look at your credit, income, and debt to determine how much you can borrow. It helps you shop confidently, knowing exactly what price range fits your budget.

When you’re comparing loan offers, don’t just look at the interest rate. Pay close attention to the Annual Percentage Rate (APR), which includes interest plus lender fees. A lower APR means a cheaper loan overall, even if the base interest rate looks slightly higher.

Key takeaway:

Understanding how home loans work gives you control over one of the biggest financial decisions of your life. Once you grasp the basics—like payment structure, interest rates, and loan terms—you can compare lenders with confidence and choose the mortgage that fits your long-term financial comfort.

First-Time Home Buyer? Unlock Your Best Loan Options.

- Understand loan basics like PITI, fixed/adjustable rates, and pre-approval to confidently compare offers.

- FHA loans are ideal for first-time buyers with modest savings (3.5% down) or lower credit scores (580+).

- Conventional loans reward strong credit (620+) and savings, potentially avoiding PMI with a 20% down payment.

- VA and USDA loans offer 0% down and competitive rates for eligible military personnel/veterans or rural/suburban buyers.

- Choose a loan that aligns with your financial goals and future plans, comparing APR, closing costs, and overall long-term value.

FHA Loans: The Most Popular Option for First-Time Buyers

For many first-time homebuyers, an FHA loan—backed by the Federal Housing Administration—is the easiest and most accessible route to homeownership. It’s specifically designed for people with modest incomes or imperfect credit who still want to own a home.

What makes FHA loans stand out is their flexibility. You can qualify with a credit score as low as 580 and a down payment as low as 3.5%. That means if you’re buying a $300,000 home, you’d only need about $10,500 upfront. This feature alone helps thousands of first-time buyers every year step into homes sooner than they ever thought possible.

Main benefits of FHA loans

| Feature | Advantage for Buyers |

| Low Down Payment | As little as 3.5% down |

| Flexible Credit Requirements | Accepts lower credit scores (580+) |

| Higher Debt-to-Income Ratio | Ideal for those managing other debts |

| Assumable Loans | Future buyers can take over your mortgage rate. |

While the benefits are clear, there are trade-offs. Mortgage Insurance Premiums (MIP) are monthly fees and upfront expenses for FHA loans. These protect the lender but add to your total cost. However, if you refinance into a conventional loan later, you can remove that insurance once you’ve built enough equity.

Another advantage of FHA loans is their lenient approval process. Lenders working with FHA guidelines often consider alternative forms of credit history, such as consistent rent or utility payments. That’s a huge plus for younger buyers who may not yet have an extensive credit history.

When an FHA loan makes sense

- You’re buying your first home and have limited savings.

- Your credit score is below 650.

- You expect your income to increase in the coming years.

- You’re okay with paying mortgage insurance in exchange for easier qualification.

Key takeaway:

FHA loans make homeownership achievable for first-time buyers with low savings or fair credit. They open the door to owning a home sooner, with manageable requirements and supportive terms that grow with you over time.

Conventional Loans: When You’ve Got Strong Credit and Savings

If you’ve spent years building your credit and maintaining a steady income, a conventional loan might reward that effort with lower long-term costs. Unlike government-backed loans, conventional mortgages are financed through private lenders and follow Fannie Mae and Freddie Mac guidelines.

One of the biggest draws of a conventional loan is flexibility. You can select loan terms of 10, 15, 20, or 30 years based on your lifestyle. You can also choose between fixed and adjustable rates based on your long-term plans. And if you can afford to put down 20% or more, you’ll skip Private Mortgage Insurance (PMI) entirely—a major cost saver.

Here’s how conventional loans compare with FHA loans:

| Feature | Conventional Loan | FHA Loan |

| Minimum Down Payment | 3% | 3.5% |

| Credit Score Minimum | 620 | 580 |

| Mortgage Insurance | Only if <20% down | Required for all |

| Loan Limits | Higher in many areas | Capped by FHA guidelines |

Because conventional loans are risk-based, borrowers with higher credit scores and lower debt ratios get the best rates. This implies that your years of frugal living will eventually lead to lower monthly payments and less interest.

Tips for qualifying for a conventional loan

- Keep your credit score above 700 for optimal rates.

- Maintain a debt-to-income ratio below 43%.

- Save at least 5%–10% down if possible to reduce insurance costs.

- Shop around among multiple lenders—rates can vary by 0.25% or more.

If you’re planning to stay in your home long-term, a conventional loan often results in lower overall costs, even if the upfront requirements are slightly higher.

Key takeaway:

Conventional loans reward financial preparedness. For buyers with strong credit and solid savings, they’re often the most cost-effective way to build equity and avoid extra fees like PMI.

VA and USDA Loans: Hidden Gems for Eligible Buyers

Many first-time buyers overlook VA and USDA loans, yet they’re among the most generous and accessible programs available. These government-backed options make homeownership possible with a zero-down payment and favorable interest rates—a combination hard to beat.

VA Loans (For Veterans and Active-Duty Military)

These loans are guaranteed by the Department of Veterans Affairs (VA) for service personnel, veterans, and qualified spouses.

Benefits include:

- No down payment required.

- No monthly mortgage insurance.

- Competitive interest rates.

- Flexible qualification guidelines.

There’s typically a funding fee, which can be financed into the loan and waived for some disabled veterans. VA loans are a thank-you for service—making homeownership both attainable and affordable.

USDA Loans (For Rural and Suburban Buyers)

To encourage homeownership in rural and some suburban areas, the U.S. Department of Agriculture (USDA) provides loans.

Advantages include:

- 100% financing (no down payment).

- Below-market interest rates.

- Lenient credit score requirements (640+).

- Lower mortgage insurance than FHA loans.

Eligibility depends on both location and income limits—you can check approved areas using the USDA Property Eligibility Map.

Comparison Table

| Feature | VA Loan | USDA Loan |

| Down Payment | 0% | 0% |

| Credit Score | Flexible | 640+ |

| Location Limit | Any | Rural/Suburban |

| Mortgage Insurance | None | Required |

| For Whom | Military families | Rural households |

Key takeaway:

VA and USDA loans provide incredible value for eligible buyers. If you qualify, these options can dramatically reduce upfront costs and make homeownership accessible without the heavy financial lift of traditional loans.

Choosing the Right Loan for Your Financial Future

Choosing a mortgage isn’t just about finding the lowest rate—it’s about selecting a loan that aligns with your financial comfort and future goals. What’s right for one buyer might not suit another, and that’s perfectly okay.

Questions to ask yourself

- How long do I plan to live in this home?

- Can I handle fluctuations in my monthly payments if rates change?

- Am I prioritizing a low upfront cost or long-term savings?

- Do I have savings set aside for repairs or emergencies?

When comparing loans, look beyond the advertised rate. Review the APR, closing costs, origination fees, and any prepayment penalties. Even small differences can add up over the life of a loan.

If you’re unsure, consider speaking with a HUD-approved housing counselor or a trusted lender to break down the numbers. And remember, your first mortgage doesn’t have to be your last. As your credit improves and equity grows, you can refinance to secure better terms later.

Key takeaway:

The right home loan is the one that supports your lifestyle and future stability. Taking the time to compare your options and understand your comfort level will lead to smarter financial decisions and peace of mind.

Frequently Asked Questions

What credit score do I need to buy a home?

Most FHA loans allow scores as low as 580, while conventional loans generally require a score of 620 or higher.

How much should I save for a down payment?

Many buyers put down 3%–5%, but you can buy with zero down through VA or USDA loans.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a quick estimate. Pre-approval requires documents and verifies how much you can actually borrow.

Can I use gift money for my down payment?

Yes, most loan programs accept gift funds from family, as long as you provide a letter confirming it’s not a loan.

Can I still buy a home if I have student loans?

Yes, as long as your debt-to-income ratio stays within acceptable limits. Many lenders work with borrowers who have student debt.

Conclusion

Becoming a homeowner for the first time isn’t just about money—it’s about creating stability, building equity, and finding a place that truly feels like yours. The right home loan can make that journey smoother and less stressful. Every step you take will get you closer to the house you’ve worked so hard for, whether you choose an FHA loan for flexibility, a conventional loan for long-term savings, or a VA or USDA loan for its incomparable rates.

Recommended Reading

The Advantages of Using a Mortgage Broker

Purchasing a home is one of the most thrilling life milestones, but it can also be daunting. Between comparing rates, understanding loan types, and keeping track of countless documents, the process can feel like a maze. That’s where a mortgage broker becomes invaluable. They serve as your guide, connecting you with the right lenders, helping […]

How to Qualify for a Mortgage with a Low Credit Score

Buying a home is one of life’s biggest milestones—but when your credit score isn’t where you want it to be, it can feel like an impossible dream. The truth is, getting a mortgage with a low credit score is absolutely possible. It just takes the right preparation, knowledge, and strategy. This guide explains how lenders […]

How to Choose the Best Lender for Your Home Loan

Buying a home isn’t just about finding the perfect property—it’s about choosing the right financial partner to make it possible. Your lender shapes everything from your monthly payment to how confident you feel when signing those final papers. The wrong fit can cost you thousands or leave you feeling anxious about every update. The right […]

How to Apply for a Home Loan Step by Step

Buying a home is exciting, but applying for a home loan can feel overwhelming if you don’t know where to begin. Between checking your credit score, gathering paperwork, and waiting for approval, there are plenty of moving parts. The good news is that once you understand the process, it becomes much less stressful. Here’s a […]

Leave a Reply