The Best Home Loan Options for First-Time Buyers

One of life’s greatest achievements is purchasing your first house, but it can also be one of the scariest. Between learning new terminology, saving for a down payment, and understanding the various loan options, many first-time buyers feel overwhelmed before they even begin. The truth is, finding the right home loan doesn’t have to be complicated. With the right knowledge and preparation, you can align your financial goals with the loan that best fits your lifestyle and long-term plans.

This guide breaks down the best home loan options designed for first-time buyers, so you can make an informed, confident decision about financing your new home.

Understanding How Home Loans Work Before You Dive In

Buying a home isn’t just about choosing the right property—it’s about understanding the financial foundation that makes homeownership possible—for first-time buyers, grasping the basics of how home loans work can prevent future stress and help you spot a good deal when you see one.

Buying a home isn’t just about choosing the right property—it’s about understanding the financial foundation that makes homeownership possible—for first-time buyers, grasping the basics of how home loans work can prevent future stress and help you spot a good deal when you see one.

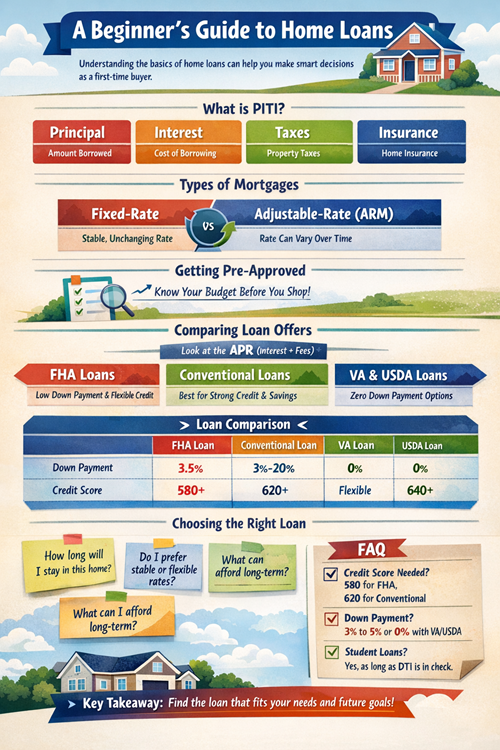

A home loan (mortgage) is a long-term agreement where a lender provides funds for you to purchase a home, and you agree to repay that money—plus interest—over time. The majority of home loans have terms between 15 and 30 years, and each monthly payment usually consists of four essential elements, commonly known as PITI:

- Principal: The amount of money borrowed to buy the home.

- Interest: The cost of borrowing that money, expressed as a percentage.

- Taxes: Your local government collects property taxes.

- Insurance: Homeowners insurance that protects against damage or loss.

There are two main types of mortgages:

- For fixed-rate mortgages, the interest rate doesn’t change during the course of the loan. For purchasers who like consistency and intend to live in their house for a long time, these are perfect.

- Adjustable-rate mortgages (ARMs), whose rates can change after an initial period. ARMs often start with a lower rate, which makes them appealing for buyers planning to sell or refinance within a few years.

Before you even start house hunting, it’s smart to get pre-approved for a loan. Pre-approval isn’t just a rough estimate—it’s a detailed look at your credit, income, and debt to determine how much you can borrow. It helps you shop confidently, knowing exactly what price range fits your budget.

When you’re comparing loan offers, don’t just look at the interest rate. Pay close attention to the Annual Percentage Rate (APR), which includes interest plus lender fees. A lower APR means a cheaper loan overall, even if the base interest rate looks slightly higher.

Key takeaway:

Understanding how home loans work gives you control over one of the biggest financial decisions of your life. Once you grasp the basics—like payment structure, interest rates, and loan terms—you can compare lenders with confidence and choose the mortgage that fits your long-term financial comfort.

First-Time Home Buyer? Unlock Your Best Loan Options.

- Understand loan basics like PITI, fixed/adjustable rates, and pre-approval to confidently compare offers.

- FHA loans are ideal for first-time buyers with modest savings (3.5% down) or lower credit scores (580+).

- Conventional loans reward strong credit (620+) and savings, potentially avoiding PMI with a 20% down payment.

- VA and USDA loans offer 0% down and competitive rates for eligible military personnel/veterans or rural/suburban buyers.

- Choose a loan that aligns with your financial goals and future plans, comparing APR, closing costs, and overall long-term value.

FHA Loans: The Most Popular Option for First-Time Buyers

For many first-time homebuyers, an FHA loan—backed by the Federal Housing Administration—is the easiest and most accessible route to homeownership. It’s specifically designed for people with modest incomes or imperfect credit who still want to own a home.

What makes FHA loans stand out is their flexibility. You can qualify with a credit score as low as 580 and a down payment as low as 3.5%. That means if you’re buying a $300,000 home, you’d only need about $10,500 upfront. This feature alone helps thousands of first-time buyers every year step into homes sooner than they ever thought possible.

Main benefits of FHA loans

| Feature | Advantage for Buyers |

| Low Down Payment | As little as 3.5% down |

| Flexible Credit Requirements | Accepts lower credit scores (580+) |

| Higher Debt-to-Income Ratio | Ideal for those managing other debts |

| Assumable Loans | Future buyers can take over your mortgage rate. |

While the benefits are clear, there are trade-offs. Mortgage Insurance Premiums (MIP) are monthly fees and upfront expenses for FHA loans. These protect the lender but add to your total cost. However, if you refinance into a conventional loan later, you can remove that insurance once you’ve built enough equity.

Another advantage of FHA loans is their lenient approval process. Lenders working with FHA guidelines often consider alternative forms of credit history, such as consistent rent or utility payments. That’s a huge plus for younger buyers who may not yet have an extensive credit history.

When an FHA loan makes sense

- You’re buying your first home and have limited savings.

- Your credit score is below 650.

- You expect your income to increase in the coming years.

- You’re okay with paying mortgage insurance in exchange for easier qualification.

Key takeaway:

FHA loans make homeownership achievable for first-time buyers with low savings or fair credit. They open the door to owning a home sooner, with manageable requirements and supportive terms that grow with you over time.

Conventional Loans: When You’ve Got Strong Credit and Savings

If you’ve spent years building your credit and maintaining a steady income, a conventional loan might reward that effort with lower long-term costs. Unlike government-backed loans, conventional mortgages are financed through private lenders and follow Fannie Mae and Freddie Mac guidelines.

One of the biggest draws of a conventional loan is flexibility. You can select loan terms of 10, 15, 20, or 30 years based on your lifestyle. You can also choose between fixed and adjustable rates based on your long-term plans. And if you can afford to put down 20% or more, you’ll skip Private Mortgage Insurance (PMI) entirely—a major cost saver.

Here’s how conventional loans compare with FHA loans:

| Feature | Conventional Loan | FHA Loan |

| Minimum Down Payment | 3% | 3.5% |

| Credit Score Minimum | 620 | 580 |

| Mortgage Insurance | Only if <20% down | Required for all |

| Loan Limits | Higher in many areas | Capped by FHA guidelines |

Because conventional loans are risk-based, borrowers with higher credit scores and lower debt ratios get the best rates. This implies that your years of frugal living will eventually lead to lower monthly payments and less interest.

Tips for qualifying for a conventional loan

- Keep your credit score above 700 for optimal rates.

- Maintain a debt-to-income ratio below 43%.

- Save at least 5%–10% down if possible to reduce insurance costs.

- Shop around among multiple lenders—rates can vary by 0.25% or more.

If you’re planning to stay in your home long-term, a conventional loan often results in lower overall costs, even if the upfront requirements are slightly higher.

Key takeaway:

Conventional loans reward financial preparedness. For buyers with strong credit and solid savings, they’re often the most cost-effective way to build equity and avoid extra fees like PMI.

VA and USDA Loans: Hidden Gems for Eligible Buyers

Many first-time buyers overlook VA and USDA loans, yet they’re among the most generous and accessible programs available. These government-backed options make homeownership possible with a zero-down payment and favorable interest rates—a combination hard to beat.

VA Loans (For Veterans and Active-Duty Military)

These loans are guaranteed by the Department of Veterans Affairs (VA) for service personnel, veterans, and qualified spouses.

Benefits include:

- No down payment required.

- No monthly mortgage insurance.

- Competitive interest rates.

- Flexible qualification guidelines.

There’s typically a funding fee, which can be financed into the loan and waived for some disabled veterans. VA loans are a thank-you for service—making homeownership both attainable and affordable.

USDA Loans (For Rural and Suburban Buyers)

To encourage homeownership in rural and some suburban areas, the U.S. Department of Agriculture (USDA) provides loans.

Advantages include:

- 100% financing (no down payment).

- Below-market interest rates.

- Lenient credit score requirements (640+).

- Lower mortgage insurance than FHA loans.

Eligibility depends on both location and income limits—you can check approved areas using the USDA Property Eligibility Map.

Comparison Table

| Feature | VA Loan | USDA Loan |

| Down Payment | 0% | 0% |

| Credit Score | Flexible | 640+ |

| Location Limit | Any | Rural/Suburban |

| Mortgage Insurance | None | Required |

| For Whom | Military families | Rural households |

Key takeaway:

VA and USDA loans provide incredible value for eligible buyers. If you qualify, these options can dramatically reduce upfront costs and make homeownership accessible without the heavy financial lift of traditional loans.

Choosing the Right Loan for Your Financial Future

Choosing a mortgage isn’t just about finding the lowest rate—it’s about selecting a loan that aligns with your financial comfort and future goals. What’s right for one buyer might not suit another, and that’s perfectly okay.

Questions to ask yourself

- How long do I plan to live in this home?

- Can I handle fluctuations in my monthly payments if rates change?

- Am I prioritizing a low upfront cost or long-term savings?

- Do I have savings set aside for repairs or emergencies?

When comparing loans, look beyond the advertised rate. Review the APR, closing costs, origination fees, and any prepayment penalties. Even small differences can add up over the life of a loan.

If you’re unsure, consider speaking with a HUD-approved housing counselor or a trusted lender to break down the numbers. And remember, your first mortgage doesn’t have to be your last. As your credit improves and equity grows, you can refinance to secure better terms later.

Key takeaway:

The right home loan is the one that supports your lifestyle and future stability. Taking the time to compare your options and understand your comfort level will lead to smarter financial decisions and peace of mind.

Frequently Asked Questions

What credit score do I need to buy a home?

Most FHA loans allow scores as low as 580, while conventional loans generally require a score of 620 or higher.

How much should I save for a down payment?

Many buyers put down 3%–5%, but you can buy with zero down through VA or USDA loans.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a quick estimate. Pre-approval requires documents and verifies how much you can actually borrow.

Can I use gift money for my down payment?

Yes, most loan programs accept gift funds from family, as long as you provide a letter confirming it’s not a loan.

Can I still buy a home if I have student loans?

Yes, as long as your debt-to-income ratio stays within acceptable limits. Many lenders work with borrowers who have student debt.

Conclusion

Becoming a homeowner for the first time isn’t just about money—it’s about creating stability, building equity, and finding a place that truly feels like yours. The right home loan can make that journey smoother and less stressful. Every step you take will get you closer to the house you’ve worked so hard for, whether you choose an FHA loan for flexibility, a conventional loan for long-term savings, or a VA or USDA loan for its incomparable rates.

Recommended Reading

The Advantages of Using a Mortgage Broker

Purchasing a home is one of the most thrilling life milestones, but it can also be daunting. Between comparing rates, understanding loan types, and keeping track of countless documents, the process can feel like a maze. That’s where a mortgage broker becomes invaluable. They serve as your guide, connecting you with the right lenders, helping […]

How to Qualify for a Mortgage with a Low Credit Score

Buying a home is one of life’s biggest milestones—but when your credit score isn’t where you want it to be, it can feel like an impossible dream. The truth is, getting a mortgage with a low credit score is absolutely possible. It just takes the right preparation, knowledge, and strategy. This guide explains how lenders […]

How to Choose the Best Lender for Your Home Loan

Buying a home isn’t just about finding the perfect property—it’s about choosing the right financial partner to make it possible. Your lender shapes everything from your monthly payment to how confident you feel when signing those final papers. The wrong fit can cost you thousands or leave you feeling anxious about every update. The right […]

How to Apply for a Home Loan Step by Step

Buying a home is exciting, but applying for a home loan can feel overwhelming if you don’t know where to begin. Between checking your credit score, gathering paperwork, and waiting for approval, there are plenty of moving parts. The good news is that once you understand the process, it becomes much less stressful. Here’s a […]

The Advantages of Using a Mortgage Broker

<?xml encoding=”UTF-8″>

Purchasing a home is one of the most thrilling life milestones, but it can also be daunting. Between comparing rates, understanding loan types, and keeping track of countless documents, the process can feel like a maze. That’s where a mortgage broker becomes invaluable. They serve as your guide, connecting you with the right lenders, helping you secure better rates, and making the process far less stressful.

Mortgage Brokers Give You Access to More Lenders and Loan Options

Choosing a mortgage isn’t a one-size-fits-all decision. Each borrower’s circumstances are different, and the ideal loan is determined by factors such as credit score, steady income, down payment, and long-term objectives. The capacity of a mortgage broker to connect you with a larger network of lenders and provide you with more possibilities than you might discover on your own is the main benefit of working with one.

When you walk into a bank, you’re limited to that institution’s loan products. A mortgage broker, however, works with dozens of lenders—from large national banks to boutique mortgage companies and private lenders. This gives you flexibility and choice, which are key to securing favorable terms.

Here’s what that expanded access means in practice:

Types of Lenders: Mortgage Brokers Connect You With

- Traditional Banks: Established institutions with competitive fixed and adjustable-rate loans.

- Credit Unions: Often provide lower fees and flexible lending criteria for members.

- Online Lenders: Streamlined applications with potentially lower interest rates.

- Private or Non-Traditional Lenders: Ideal for self-employed borrowers or those with unique financial backgrounds.

Because brokers understand each lender’s preferences and requirements, they can match you with the right fit from the start. Instead of submitting applications blindly, your broker pinpoints lenders who are more likely to approve you based on your financial profile.

Another advantage is customization. A broker can tailor loan solutions for your goals—whether that’s a lower down payment, shorter loan term, or adjustable rate. This flexibility is especially useful for first-time buyers or anyone looking to refinance under specific conditions.

Key Takeaway: Working with a mortgage broker gives you more lender choices, better customization, and a higher chance of finding a mortgage that truly fits your lifestyle and financial goals.

They Can Save You Time and Simplify the Process

Securing a mortgage involves more than filling out an application—it’s a full-scale process that includes verifying income, evaluating credit, comparing lenders, and coordinating appraisals and closings. Managing all of that on your own can quickly become overwhelming. Mortgage brokers streamline the process from start to finish, saving you hours of research and paperwork.

When you partner with a broker, they act as the central point of contact between you, your lender, and other professionals involved in your home purchase. They collect your financial documents once and use them to apply to multiple lenders. This eliminates redundant paperwork and reduces delays.

How a Broker Simplifies the Mortgage Process

- Prequalification: Brokers analyze your finances and estimate what loan amount you can afford.

- Application Management: They handle all the forms, documents, and lender communications.

- Rate Comparison: Brokers evaluate offers from multiple lenders to identify the most cost-effective one.

- Follow-ups: They monitor your loan’s progress, address issues, and keep you informed every step of the way.

- Closing Coordination: Brokers ensure your loan closes on time by aligning all final details between you, the lender, and your agent.

Beyond convenience, this level of organization helps prevent mistakes. Many loan delays stem from missing paperwork or miscommunication, and brokers are skilled at catching them early. Their efficiency not only saves you time but can also make your offer more competitive in fast-moving housing markets.

For busy professionals or families trying to stick to a schedule, this hands-on management is invaluable. You can focus on preparing for your move or negotiating your home purchase while your broker handles the heavy lifting.

Key Takeaway: A mortgage broker saves you time and energy by managing the entire mortgage process, keeping it organized, efficient, and stress-free.

Brokers Help You Get Better Rates and Negotiate on Your Behalf

Interest rates play a massive role in your financial future. Even a small difference—say, 0.25%—can save you thousands over the life of your loan. Mortgage brokers are experts at comparing rates, identifying hidden fees, and negotiating terms to get you the best possible deal.

Unlike banks, which offer only their in-house rates, brokers have access to wholesale rates from a variety of lenders. These rates are often lower because brokers bring lenders steady business. They also understand how different lenders assess risk, allowing them to present your application in the most favorable light strategically.

Ways Brokers Help You Save Money

- Rate Comparison: Brokers instantly compare current rates across multiple lenders.

- Negotiation Power: Their relationships with lenders can lead to fee reductions or special offers.

- Wholesale Access: Brokers often secure lower rates than what retail branches advertise.

- Transparent Cost Analysis: They explain each fee—origination, underwriting, closing—to help you understand the full picture.

Beyond rates, brokers help you evaluate loan structures. Should you go with a 15-year fixed-rate loan or a 30-year adjustable-rate mortgage? A broker will break down how each affects your payments and long-term equity, giving you the clarity to make an informed choice.

Many brokers also stay alert for market changes. If rates drop before your loan closes, they can work to lock in the lower rate or renegotiate your terms.

Key Takeaway: A skilled mortgage broker doesn’t just find you a loan—they use industry insight and negotiation power to secure better rates and save you money over time.

They Offer Expert Guidance and Personalized Support

Buying a home is emotional. You’re excited about new possibilities but nervous about long-term financial commitments. Mortgage brokers bridge that gap by offering expert advice tailored to your specific situation.

They don’t just fill out forms—they educate you. They explain how credit scores affect your rate, what lenders look for in your documentation, and how to prepare your finances for approval. Their goal is to make sure you understand your mortgage, not just sign it.

What Makes Their Guidance So Valuable

- Unbiased Advice: Brokers work for you, not the bank. Their recommendations are based on your best interests.

- Financial Clarity: They translate complex mortgage terms into plain language.

- Strategic Planning: Brokers help you determine the best loan type for your income, debt, and goals.

- Continuous Support: They stay involved from pre-approval through closing, making sure no detail is missed.

This kind of personalized support is especially valuable for first-time homebuyers. Instead of feeling like you’re navigating a maze of terms and rates alone, you have someone breaking everything down and ensuring you’re comfortable at every step.

Because brokers rely heavily on reputation and client referrals, they’re motivated to deliver excellent service. They take time to understand your story and ensure your mortgage complements your long-term financial well-being.

Key Takeaway: Mortgage brokers act as trusted advisors, offering personal, expert guidance that empowers you to make confident, well-informed decisions.

Mortgage Brokers Can Help You Overcome Unique Financial Challenges

Life doesn’t always follow a straight path. You may be self-employed, have recently changed jobs, or have less-than-perfect credit. Traditional banks may see those situations as red flags—but mortgage brokers see them as challenges to solve.

Brokers specialize in finding creative solutions for borrowers who don’t fit the standard lending mold. They know which lenders are open to flexible documentation, alternative income verification, or credit repair programs.

Ways Brokers Help in Unique Situations

- Self-Employed Borrowers: Brokers connect you with lenders who accept tax returns or business statements instead of pay stubs.

- Credit Challenges: They know lenders who specialize in FHA or other programs that accommodate lower scores.

- First-Time Buyers: Brokers guide you through grants, down payment assistance, or government-backed loans.

- Refinancing: If your equity or income is limited, brokers find refinancing options that help lower payments without full requalification.

Brokers also help you understand your options in context. For example, if your credit score is currently low, they can guide you on quick ways to boost it before applying, which can significantly improve your rate.

When traditional lenders might reject you outright, a broker finds a path forward. Their connections and creativity often make homeownership possible for people who thought it was out of reach.

Key Takeaway: A mortgage broker sees beyond your credit score and job title—they focus on finding real solutions that make homeownership achievable, no matter your financial background.

Conclusion

Working with a mortgage broker transforms a complicated process into a guided, personalized experience. From connecting you with more lenders to securing better rates and simplifying every step, a broker can make buying or refinancing your home smoother and more rewarding. When you have a trusted expert advocating for your best interests, you don’t just get a mortgage—you get peace of mind.

Frequently Asked Questions

Do I have to pay a mortgage broker?

The lender, not the borrower, pays most brokers, though it’s always best to ask about compensation upfront.

Can a mortgage broker really get me a better deal?

Yes. Brokers have access to multiple lenders and often find exclusive rates or offers not available directly to consumers.

Is using a mortgage broker faster?

Usually, yes. Brokers handle communication and paperwork efficiently, which can help speed up the approval process.

Are mortgage brokers licensed?

Yes. They’re required to be licensed and comply with both state and federal regulations to protect borrowers.

Can a broker help if I have bad credit?

Absolutely. Brokers often work with lenders that specialize in loans for borrowers with lower credit scores or unique financial backgrounds.

Additional Resources

Mortgage Refinancing Explained: When and How to Do It

Refinancing your mortgage can be one of the smartest financial moves you’ll ever make—or one of the most stressful if the timing isn’t right. Knowing when and how to refinance is important, whether you want to reduce your monthly payments, pay off your loan more quickly, or access the equity in your house. Here’s everything you need to know to make a confident, informed decision.

What Is Mortgage Refinancing and How Does It Work?

A mortgage refinance substitutes your existing mortgage with a new one with alternative terms, such as a lower interest rate, a shorter payback period, or a fixed rate rather than a variable rate. The goal is to create a loan structure that better matches your financial goals today, not the ones you had when you first bought your home.

Your new lender pays off your existing mortgage when you refinance. The process resembles getting your first mortgage, including a credit check, income verification, and a home appraisal.

For example, imagine you have a 30-year mortgage at 6.5%. If current rates drop to 5%, refinancing could save you hundreds of dollars every month. Over the full loan term, that could amount to tens of thousands in savings.

Homeowners refinance for many reasons:

- To secure a lower interest rate and reduce monthly payments

- To switch from an adjustable-rate to a fixed-rate mortgage, offering more stability

- To shorten the loan term, pay off the home sooner, and save on interest

- To tap into home equity, convert some of your home’s value into cash for improvements or debt repayment

It’s essential to remember that refinancing isn’t free. Lenders charge closing costs—typically between 2% and 5% of the loan amount—and you’ll need to stay in your home long enough to recoup those costs through savings.

Key Takeaway: Refinancing lets you redesign your mortgage to better align with your current financial situation. Done wisely, it can strengthen your long-term financial security.

The Best Times to Refinance: Signs It Might Be Right for You

Timing matters in refinancing. Doing it too early—or for the wrong reasons—can cost more than it saves. The best time to refinance is when it creates a measurable financial benefit, either through savings, faster equity growth, or greater stability.

Here are the most common signs it’s a good time to refinance:

- Interest rates have dropped. If today’s rates are at least half a percent lower than your current rate, it’s worth running the numbers.

- Your credit score has improved. You may be eligible for better terms or lower rates with a higher score.

- You’ve built equity. With at least 20% equity in your home, you may remove private mortgage insurance (PMI) and reduce your payments.

- You plan to stay in your home. The longer you stay, the more time you have to recover closing costs and benefit from savings.

- You want to shorten your loan term. You can increase your equity more quickly by taking out a 15-year mortgage instead of a 30-year one.

Example:

If refinancing saves you $200 per month but costs $5,000 to close, your break-even point is 25 months ($5,000 ÷ $200 = 25). If you plan to stay longer than that, refinancing is worth considering.

Quick Refinancing Checklist:

✅ Compare your current rate to market rates

✅ Review your credit report for accuracy

✅ Calculate your break-even point

✅ Ensure you can cover closing costs upfront

Key Takeaway: The best time to refinance is when it aligns with both your current financial position and your future goals. Patience and timing can turn refinancing into a lasting win.

Types of Mortgage Refinancing Options (And Which One Fits You)

Refinancing isn’t one-size-fits-all. Different loan types cater to specific financial goals. Understanding the main options helps you choose the one that delivers the most value.

|

Type |

Best For |

What It Does |

Potential Risks |

|

Rate-and-Term Refinance |

Homeowners seeking a lower rate or shorter term |

Replaces your existing loan with one offering a lower rate, shorter term, or both |

May reset your loan timeline or involve closing costs |

|

Cash-Out Refinance |

Borrowers needing funds for renovations, education, or debt consolidation |

Let’s you borrow against home equity and receive cash |

Reduces your equity and increases total debt |

|

Cash-In Refinance |

Homeowners want to pay down principal. |

Let’s you put cash toward your loan to reduce the balance and qualify for better terms. |

Uses up liquid assets that might be needed elsewhere |

|

Streamline Refinance |

FHA or VA borrowers |

Simplifies the process by reducing paperwork and waiving appraisals |

May limit flexibility in changing loan features |

When to Choose Each:

- Choose a rate-and-term if your goal is to save money by paying a lower interest rate.

- Choose cash-out if you need capital for large expenses, but understand it increases your total debt.

- Choose cash-in if you’ve recently come into extra cash and want to secure a better rate or remove PMI.

- Choose streamline if you have a government-backed loan and want an easier, faster process.

Key Takeaway: Your refinancing decision should align with your long-term goals, not just short-term savings. Think about where you are financially—and where you want to be five years from now.

The Step-by-Step Process of Refinancing Your Mortgage

The refinancing process may seem overwhelming, but it’s easier when you break it into clear steps. Being prepared and avoiding surprises is made easier when you know what to anticipate.

Step 1: Review your financial situation.

Start by evaluating your credit score, home equity, and debt-to-income ratio. These determine your eligibility and interest rate.

Step 2: Compare lenders.

Get quotes from at least three lenders. Compare not only rates but also fees, loan terms, and closing costs.

Step 3: Apply for your refinance.

Send in your loan application along with the necessary paperwork, including bank statements, tax returns, W-2s, and pay stubs.

Step 4: Lock your rate.

If rates are favorable, ask your lender to lock your rate. This protects you from market changes during processing.

Step 5: Get your home appraised.

Lenders usually require a professional appraisal to confirm your property’s current value.

Step 6: Underwriting and approval.

Your lender reviews your file, verifies your financial details, and makes the final loan decision.

Step 7: Closing.

You’ll sign the final paperwork, pay closing costs, and start your new loan.

Tips for a Smooth Refinance:

- Organize your financial documents early.

- Respond promptly to lender requests.

- Avoid major financial changes (like opening new credit cards) during the process.

Key Takeaway: Preparation makes refinancing smoother and faster. When you plan and stay organized, you can avoid delays and secure the best deal possible.

The Hidden Costs and Common Mistakes to Avoid

Refinancing your mortgage can be one of the smartest financial choices you make—but only if you’re fully aware of the real costs involved. Many homeowners focus on getting a lower rate or smaller monthly payment, but they often underestimate the expenses and potential pitfalls that can come with the process. Understanding what you’re paying for and what to avoid helps you make a decision that genuinely improves your financial situation instead of setting you back.

1. Common Hidden Costs You Might Overlook

Refinancing can result in long-term financial savings, but it may entail substantial upfront costs. Some of the most common expenses include:

- Closing costs: 2% to 5% of the entire loan amount, on average. For example, on a $300,000 mortgage, you could pay between $6,000 and $15,000.

- Appraisal fees: Lenders typically require a new appraisal to confirm your home’s market value. Expect to pay around $400 to $700.

- Loan origination fees: These are the fees the lender charges to process your application and can range from 0.5% to 1% of the loan amount.

- Title search and insurance: These protect the lender’s ownership interest and usually cost a few hundred dollars.

- Prepayment penalties: Some mortgages charge you a fee for paying off your loan early, which can erase part of your refinancing savings.

It’s wise to ask your lender for a Loan Estimate—a standardized form that breaks down all costs and fees. This document helps you compare multiple offers side by side so you know exactly what you’re paying for.

2. Common Mistakes That Could Cost You Thousands

Even when refinancing seems like an obvious choice, rushing into it can lead to mistakes that eat into your savings. The most frequent missteps include:

- Refinancing too often. Each refinance resets your loan term, meaning you could spend more years paying interest.

- Chasing the lowest rate. A slightly lower interest rate isn’t worth it if the fees outweigh the savings.

- Not calculating the break-even point. Always know how long it’ll take to recover your closing costs through monthly savings.

- Failing to compare lenders. Interest rates, fees, and service quality vary widely between lenders. Shopping around is essential.

- Ignoring how long you’ll stay in the home. If you plan to sell within a couple of years, the savings may not justify the upfront costs.

3. How to Protect Yourself Financially

Before committing, use a refinance calculator to estimate potential savings. Review your long-term plans—if you’re planning to move or need flexibility for future expenses, refinancing might not be worth the commitment. Also, negotiate closing costs when possible. Some lenders may reduce or roll them into your loan if you have strong credit and good equity.

Key Takeaway: Refinancing isn’t just about getting a lower rate—it’s about making sure the numbers work in your favor. Understanding all the costs, carefully comparing offers, and avoiding common mistakes ensures your refinance strengthens your financial future rather than adding unnecessary debt.

Conclusion

Mortgage refinancing can be an incredible financial strategy when the timing and purpose align. It’s not just about lowering rates—it’s about building long-term financial stability, gaining flexibility, and shaping a mortgage that fits your life today. When done thoughtfully, refinancing can ease your financial burden and open new opportunities for the future.

FAQs

How often can I refinance my mortgage?

There’s no legal limit, but most lenders recommend waiting at least six months between refinances.

Can I refinance with bad credit?

Yes, but you may face higher interest rates. Improving your credit first usually leads to better options.

How long does refinancing take?

Most refinances close in about 30 to 45 days, depending on your lender and how quickly you provide documentation.

What’s a break-even point?

It’s how long it takes for your refinance savings to cover your upfront costs.

Is refinancing always worth it?

Not necessarily. It’s only worth it if you’ll save more over time than you spend on fees.

Additional Resources

How to Refinance Your Mortgage and Save Money

<?xml encoding=”UTF-8″>

Refinancing your mortgage can be one of the most powerful ways to take charge of your finances. It’s not just about lowering your interest rate—it’s about freeing up money, building security, and reshaping how you manage your biggest investment: your home. Knowing how refinancing works can help you make confident, well-informed decisions, whether your objective is to access your home’s equity, reduce monthly payments, or shorten your loan term.

What Does It Really Mean to Refinance Your Mortgage

Understanding the Basics

Your existing home loan is replaced with a new one—ideally, one with better terms—when you refinance your mortgage. The new loan pays off your old mortgage entirely, and you begin making payments based on the new agreement. People refinance for many reasons, but the goal is usually the same: save money, build financial flexibility, or both.

Refinancing can make sense if interest rates have dropped, your credit score has improved, or your financial goals have changed. It’s also a good option if you want to switch loan types or remove private mortgage insurance (PMI).

Main Types of Refinancing

- Rate-and-term refinance: Replaces your existing loan with a new one that has a different rate, term, or both—most commonly used to lower payments or pay off the loan faster.

- Cash-out refinance: Enables you to borrow money against the equity in your house to pay for debt consolidation, school, or improvements.

- Streamline refinance: A faster, lower-documentation option available for FHA, VA, or USDA loans.

Common Reasons Homeowners Refinance

| Reason | Benefit |

| Lower interest rate | Reduces monthly payments and total interest paid |

| Shorter term | Builds equity faster and reduces total loan cost |

| Change loan type | Offers more stability (switch from ARM to fixed rate) |

| Cash-out | Provides access to home equity for large expenses |

While refinancing offers big financial advantages, it’s not always ideal. Each refinance comes with closing costs—usually 2–5% of your loan balance. If you’re planning to sell your home soon, you might not save enough to justify those costs.

Key takeaway: Refinancing is about financial strategy, not quick savings—it works best when aligned with your long-term goals.

Signs It’s the Right Time to Refinance Your Home Loan

Recognizing the Right Opportunity

The success of your refinance can be greatly impacted by timing. Knowing when to act ensures you don’t miss a valuable opportunity—or refinance at the wrong moment.

Here are signs it may be time to refinance:

- Interest rates have dropped significantly.

If rates are 0.5% to 1% lower than your current rate, you can save a meaningful amount over the loan’s lifetime.

- Your credit score has improved.

A stronger score can qualify you for lower interest rates or eliminate costly mortgage insurance premiums.

- You’ve built more equity in your home.

Home values often increase over time. Once you reach 20% equity, you may access better terms and avoid PMI.

- You want to change your loan term or structure.

You can pay off your mortgage more quickly by moving from a 30-year loan to a 15-year term.

- You’re planning to stay in your home long-term.

Refinancing only makes sense if you’ll remain in your home long enough to recoup closing costs through monthly savings.

The Role of Market and Personal Timing

Market timing matters, but your personal financial health matters just as much. If you’ve recently paid down debt, received a raise, or improved your credit history, lenders are more likely to offer you favorable refinancing terms.

You can also look at the “break-even” point. This tells you how long it’ll take for your savings to outweigh the upfront refinancing costs. For instance, if you spend $5,000 in closing costs and save $250 a month, you’ll break even in 20 months.

Key takeaway: The best time to refinance is when market rates and your personal finances align to create long-term savings.

How to Calculate Whether Refinancing Will Actually Save You Money

Understanding the Math

Refinancing sounds appealing, but not every refinance results in savings. The key is to do the math and ensure that your long-term financial benefits outweigh the upfront costs.

Start by collecting three details from your current loan:

- Remaining loan balance

- Interest rate

- Years left on the loan

Then, compare those with the new loan terms:

- New interest rate

- New term length

- Estimated closing costs

Using a refinance calculator or spreadsheet can help visualize the difference.

Example Calculation

| Item | Current Loan | New Loan |

| Balance | $300,000 | $300,000 |

| Interest Rate | 6.5% | 5.0% |

| Monthly Payment | $1,896 | $1,610 |

| Monthly Savings | $286 | |

| Break-even Point | About 20 months |

In this example, if refinancing costs $5,500, it takes 20 months to break even. After that, you save $286 every month.

Other Factors to Consider

- Loan term reset: Refinancing to another 30-year term could extend your debt timeline.

- Property taxes and insurance: These stay the same, but always include them for a realistic budget.

- Private mortgage insurance: If you’ve built enough equity, refinancing may eliminate PMI.

Key takeaway: Refinancing is worth it only when your long-term savings exceed the upfront costs—always calculate before signing.

Common Refinancing Mistakes Homeowners Regret

Lessons Learned from Costly Missteps

Refinancing can be a game-changer, but only if it’s done thoughtfully. Many homeowners rush into refinancing because they hear about low interest rates or see friends saving money, only to find out later that they didn’t actually come out ahead. The truth is, refinancing isn’t a one-size-fits-all solution. It requires clear financial goals, careful timing, and an understanding of the long-term tradeoffs.

One of the biggest mistakes homeowners make is focusing only on the monthly payment. While lowering your payment sounds great, it doesn’t always mean you’re saving money. If you extend your loan back to 30 years when you’ve already paid 10 years off, you’ll likely end up paying more in total interest—even at a lower rate. That’s why you should always look at the overall cost of the loan, not just the monthly payment.

Another common misstep is failing to compare multiple lenders. Rates and fees can vary dramatically between financial institutions. Some lenders advertise a lower rate but charge high closing costs, while others may offer fewer fees but a slightly higher rate. Comparing at least three Loan Estimates side-by-side helps you see the true value of each offer.

Homeowners also often forget to calculate the break-even point. This is the point where the money you save each month equals the amount you spent on refinancing. If you plan to move before you reach that point, refinancing might not make financial sense.

How to Avoid These Mistakes

- Ask lenders to explain all fees upfront.

- Avoid extending your loan term unless necessary.

- Use refinance calculators to project real long-term savings.

- Don’t refinance too frequently—it can reset your debt timeline and cost more in the end.

- Review your credit and income before applying to ensure you qualify for the best possible rate.

Refinancing is about patience and precision. If you approach it thoughtfully, it can strengthen your financial foundation rather than weaken it.

Key takeaway: Smart refinancing means looking beyond quick savings and understanding the long-term impact—avoid shortcuts, and your wallet will thank you.

Step-by-Step Guide to Refinancing Your Mortgage Smoothly

A Practical Roadmap to Stress-Free Refinancing

Refinancing your mortgage doesn’t have to be confusing or stressful. When you know exactly what steps to take, you’ll not only save time but also secure the best deal available. Think of it as a structured financial tune-up—organized, deliberate, and rewarding when done right.

The Step-by-Step Process

- Check your credit report.

Before you even reach out to a lender, pull your credit report from all three major bureaus. Make sure there are no errors and that your balances are low. Even a small improvement in your score can lead to a better rate.

- Define your goal.

Are you refinancing to lower monthly payments, shorten your term, or access your home’s equity? Knowing your “why” keeps your decisions focused and helps lenders tailor the right loan options for you.

- Shop multiple lenders.

Don’t settle for the first offer. Collect at least three Loan Estimates from different lenders. Keep an eye on the annual percentage rate, which accounts for both closing fees and the interest rate.

- Prepare your documentation.

Gather pay stubs, W-2s, recent tax returns, bank statements, and proof of assets. Having these ready speeds up the approval process and shows lenders you’re organized.

- Lock in your rate.

Once you find a rate that meets your goals, lock it in. This shields you against market swings by guaranteeing your rate for a predetermined period, usually 30 to 60 days.

- Home appraisal and underwriting.

To determine your house’s current market value, your lender will request an appraisal. Meanwhile, underwriting reviews your financials to ensure you meet all requirements.

- Closing the loan.

During closing, you’ll sign final documents, pay any required fees, and officially replace your old loan with the new one.

- Confirm your first payment date.

Double-check your loan statement to ensure your first payment is correct and that any automatic payments (if any) are properly transferred.

Extra Tips for a Smooth Experience

- Keep your finances stable throughout the process. Steer clear of making big purchases or creating additional credit lines.

- Stay in touch with your lender—they’ll let you know if they need additional information.

- Ask about potential rate float-down options if rates drop before closing.

When done correctly, refinancing should feel empowering, not overwhelming. Preparation and awareness are your best tools for making the process smooth and beneficial.

Key takeaway: A successful refinance depends on clarity, organization, and proactive communication—treat it like a financial reset designed to simplify your future.

Conclusion

Refinancing isn’t just about getting a lower rate—it’s about building a stronger financial foundation. When done strategically, it can reduce your debt faster, improve your cash flow, and give you more control over your financial future. The key is to act with clarity, run the numbers, and choose a path that supports your long-term peace of mind.

FAQs

Does refinancing hurt my credit score?

It can slightly lower your score because of hard credit inquiries, but the impact is usually small and temporary.

How often can I refinance my mortgage?

There’s no limit, but frequent refinancing can eat away at your savings through repeated closing costs.

What credit score do I need to refinance?

Although a score of 620 or above is usually necessary, it is the most competitive.

Prices are obtained with a score of 700 or higher.

Can an FHA loan be converted into a traditional one?

Yes, many homeowners refinance FHA loans into conventional loans to remove mortgage insurance once they have enough equity.

How long does refinancing take?

Most refinances close within 30 to 45 days, depending on the lender’s speed and appraisal timelines.

Additional Resources

How to Qualify for a Mortgage with a Low Credit Score

<?xml encoding=”UTF-8″>

Buying a home is one of life’s biggest milestones—but when your credit score isn’t where you want it to be, it can feel like an impossible dream. The truth is, getting a mortgage with a low credit score is absolutely possible. It just takes the right preparation, knowledge, and strategy.

This guide explains how lenders think, what programs can help, and what you can do right now to improve your chances of approval.

What Counts as a “Low” Credit Score When Applying for a Mortgage

A “low” credit score doesn’t have one universal definition—it depends on the lender, the loan program, and your overall financial situation. Still, most lenders use the FICO score, which ranges from 300 to 850, as their benchmark for determining borrower risk.

Understanding Credit Score Ranges

| Credit Range | Rating | What It Means for Borrowers |

| 740–850 | Excellent | Qualifies for the best interest rates and lowest fees |

| 700–739 | Good | Strong approval chances with favorable terms |

| 620–699 | Fair | Eligible for most conventional mortgages |

| 580–619 | Poor | May qualify for FHA or other government-backed loans |

| Below 580 | Very Poor | Limited options often require a higher down payment |

Most conventional lenders consider 620 the minimum score for approval. However, that number doesn’t tell the whole story. For example, FHA loans—which are backed by the Federal Housing Administration—allow borrowers with credit scores as low as 500 to put down 10%. Borrowers with a 580+ score can qualify with only 3.5% down.

Why Lenders Care About Credit Scores

Your credit score reflects your history with debt—how reliably you’ve paid it back and how much of it you currently owe. Lenders use it to assess the risk of lending to you. A low score suggests a higher likelihood of missed payments, which increases the lender’s risk. To offset that, they may offer:

- Higher interest rates

- Larger required down payments

- Stricter income verification

But remember: lenders look at your full financial profile. Even with a lower score, you might qualify if other parts of your application—like your job history or debt-to-income ratio—look strong.

Key takeaway:

A “low” credit score isn’t a dead end—it’s a starting point. Different lenders and loan programs have different thresholds, so understanding where you fall and what options fit your range is the first step toward homeownership.

How Lenders Evaluate Risk Beyond Your Credit Score

Although your credit score is a major factor in the approval process, it is not the only one. Mortgage lenders use a more holistic view to determine if you’re capable of managing long-term debt responsibly.

Factors Lenders Consider

1. Debt-to-Income Ratio (DTI):

This ratio calculates the percentage of your total monthly income that is used for debt repayment. Although certain programs allow up to 50% with offsetting considerations, most lenders prefer a DTI below 43%.

2. Employment and Income Stability:

Lenders want to see consistent employment for at least two years, ideally with the same employer or in the same field. Freelancers and gig workers can qualify, too, but they’ll need to show steady income through tax returns or 1099 forms.

3. Down Payment Size:

A larger down payment reduces lender risk. It shows commitment and instantly builds equity. For instance, a borrower with poor credit who puts 10% down might seem more reliable than someone with great credit who puts 0% down.

4. Savings and Cash Reserves:

Having at least two to three months’ worth of mortgage payments in savings reassures lenders that you can weather unexpected costs like car repairs or medical bills.

5. Payment History and Financial Behavior:

Lenders closely review your past 12 months. Even if your score isn’t high, a recent record of on-time payments signals that your financial habits are improving.

How to Strengthen Your Overall Application

If your credit score is low, focus on showing financial consistency elsewhere.

- Pay off smaller loans first to reduce your DTI.

- Gather documents proving steady income or multiple income sources.

- Avoid taking on new debt right before applying.

- Write a short explanation letter for any past financial hardships.

This well-rounded approach helps humanize your application, allowing lenders to see beyond your numbers.

Key takeaway:

Lenders don’t just look at your score—they look at your story. A strong financial profile, with steady income, savings, and reliable payments, can outweigh a less-than-perfect credit history.

Loan Plans for Borrowers with Imperfect Credit

Not all loans are created equal. Some are specifically built for borrowers with lower credit scores or limited financial history. Understanding these programs can help you find the one that best fits your situation.

Government-Backed Loans

FHA Loans (Federal Housing Administration)

- Minimum credit score: 500–580

- Down payment: 10% for 500–579, 3.5% for 580+

- Backed by the government, making lenders more flexible

- Requires mortgage insurance (MIP), which adds to your monthly cost

- Learn more:

VA Loans (Department of Veterans Affairs)

- No official minimum credit score (lenders often require 580–620)

- No down payment required

- No private mortgage insurance (PMI)

- Exclusively for veterans, active-duty military members, and eligible spouses

- Learn more:

USDA Loans (U.S. Department of Agriculture)

- Usually requires a score of 640+

- Designed for rural or suburban buyers

- No down payment required

- There are income restrictions based on family size and region.

- Learn more: USDA Rural Development Loans

Alternative Loan Options

Non-QM (Non-Qualified Mortgage) Loans:

These are for borrowers who don’t fit traditional molds—like self-employed individuals, investors, or people recovering from credit issues. Non-QM loans often allow:

- Alternative income verification (bank statements instead of W-2s)

- Flexible credit score requirements

- Higher interest rates in exchange for flexibility

Key takeaway:

There’s no one-size-fits-all mortgage. Government-backed loans like FHA, VA, and USDA make homeownership possible even for those with lower scores, while non-QM options offer flexibility for unique financial situations.

Smart Moves to Strengthen Your Application Right Now

You don’t have to wait months to make progress—there are several practical actions you can take today to make your mortgage application stronger.

Improve Your Debt Profile

- Pay down revolving debt: Credit card balances have the biggest impact on your score. Try to keep your utilization under 30%.

- Avoid new credit inquiries: Each hard pull can reduce your score slightly, so hold off on opening new accounts.

- Consolidate high-interest debt: Consider a personal loan with a lower rate to simplify payments.

Boost Your Credibility with Lenders

- Show consistent income: Gather recent pay stubs, W-2s, or tax returns to prove financial stability.

- Add a co-borrower: Partnering with someone who has a stronger score can increase your approval chances.

- Write a letter of explanation: If you’ve had financial setbacks—like medical bills or job loss—explain them briefly and clearly.

Present a Stronger Down Payment

If possible, aim for a higher down payment than the minimum required. This not only reduces your loan amount but also shows commitment. Even an extra 2–3% can make your application stand out.

Example Table: Down Payment vs. Credit Strength

| Credit Score | Minimum Down Payment | Stronger Down Payment Recommended |

| 580–619 | 3.5% (FHA) | 5–10% |

| 500–579 | 10% | 15% |

| Below 500 | Usually ineligible | N/A |

Key takeaway:

You can make a strong impression even with a weak score. Focus on paying down debt, gathering proof of financial stability, and saving for a slightly larger down payment to boost your approval odds.

How to Rebuild Credit for Better Mortgage Terms in the Future

If you’re not ready to apply just yet—or want better terms later—now’s the perfect time to rebuild your credit. Significant progress can be achieved with even modest, regular adjustments.

Practical Credit-Building Strategies

- Pay every bill on time: Payment history makes up 35% of your credit score. Automate payments to avoid missed due dates.

- Lower your credit utilization: Keep balances under 30% of your limit; 10% or less is even better.

- Dispute errors on your report: Use AnnualCreditReport.com to check for inaccuracies and file disputes when necessary.

- Use secured credit cards: Deposit-based cards help you build credit safely without overspending.

- Keep old accounts open: Your credit history accounts for 15% of your score, so keep older accounts active.

Adopt Financial Habits that Build Momentum

- Track your credit monthly: Free tools like can help you monitor progress.

- Avoid co-signing loans: Someone else’s missed payments can drag your score down.

- Diversify your credit mix: A blend of revolving (credit cards) and installment (loans) accounts can strengthen your score.

Realistic Timeline for Improvement

| Credit Issue | Typical Recovery Time |

| Late payments | 3–6 months |

| High credit utilization | 1–3 months after paydown |

| Collection accounts | 6–12 months after resolution |

| Bankruptcy | 12–24 months for noticeable improvement |

Key takeaway:

Rebuilding credit takes patience, but every on-time payment and reduced balance moves you closer to a stronger financial future—and a better mortgage deal when you’re ready.

Conclusion

A low credit score doesn’t mean you can’t own a home. It just means you need a strategy. By understanding your options, building financial stability, and choosing the right loan program, you can qualify for a mortgage and take that exciting step toward homeownership.

Frequently Asked Questions

Can someone with a credit score of 580 purchase a home?

Yes. FHA loans often approve borrowers with scores as low as 580 if they can make a 3.5% down payment.

How much should I save for a down payment with bad credit?

You may need around 10% if your score is below 580, though requirements vary by lender.

Does applying for a mortgage lower my credit score?

Slightly, yes. Each hard inquiry may reduce your score a few points, but multiple mortgage inquiries within 45 days count as one.

Can I qualify without a credit history?

Yes. Some lenders use manual underwriting, reviewing rent, utilities, and other payment records.

How long does credit rebuilding take?

After 6 to 12 months of regular, on-time payments and responsible credit use, many borrowers experience discernible improvements.

Additional Resources

How to Raise Your Credit Score Prior to Purchasing a Home

<?xml encoding=”UTF-8″>

Buying a home is an exciting milestone, but before you start touring open houses, there’s one thing you can’t overlook—your credit score. This three-digit number tells lenders how reliable you are with money, and it plays a major role in the mortgage rates you’ll be offered. The better your score, the lower your costs over time. The encouraging part is that improving your credit score isn’t as difficult as it sounds—you need to know where to start.

Why Your Credit Score Matters More Than You Think When Buying a Home

Your credit score is crucial to the home-buying process, which is a significant milestone. It’s one of the first things lenders look at when deciding whether to approve your mortgage—and at what interest rate. Think of it as your financial reputation in numerical form.

A strong credit score (typically 740 or higher) signals that you’re reliable with money. Lenders reward that reliability with lower interest rates, smaller down payments, and access to better loan programs. On the other hand, a weaker score can make borrowing more expensive or limit your loan options entirely.

Here’s how your score affects your mortgage:

| Credit Score Range | Loan Type Accessibility | Estimated Interest Rate Impact |

| 760–850 | Excellent – access to top mortgage offers | Lowest available rates |

| 700–759 | Good – broad loan options | Slightly higher rates |

| 650–699 | Fair – FHA or special programs likely | Moderate rate increase |

| 600–649 | Poor – limited loan access | Noticeably higher rates |

| Below 600 | Very Poor – high-risk borrower | Difficult approval or denial |

For example, if you borrow $300,000 at 6.5% instead of 8.5%, you could save nearly $400 a month—or more than $140,000 over 30 years. That’s why lenders weigh credit scores so heavily.

A high score also helps with mortgage insurance costs, faster approvals, and better negotiation power. Sellers may view you as a more reliable buyer, especially in competitive housing markets.

Key takeaway: Treat your credit score like a financial passport. The higher it is, the smoother your path to homeownership will be.

Breaking Down What Really Impacts Your Credit Score

Understanding what shapes your credit score is the first step toward improving it. Many people focus only on paying bills on time, but there’s much more to it. The score is calculated using five major components, each carrying its own weight.

| Factor | Weight on Score | What It Means | How to Improve It |

| Payment History | 35% | How consistently you make on-time payments | Always pay by the due date; set up autopay or reminders |

| Credit Utilization | 30% | The ratio of used credit to your total limit | Keep usage under 30%; aim for 10% for top performance |

| Length of Credit History | 15% | How long have your accounts been active | Keep old accounts open; don’t close your oldest credit cards |

| New Credit Inquiries | 10% | How often do you apply for new credit | Limit new credit applications before applying for a mortgage |

| Credit Mix | 10% | Variety of credit types (cards, loans, etc.) | Maintain a healthy mix if possible, but don’t overextend |

It’s also important to check your credit reports for errors. Even a small mistake—like an incorrect late payment—can drop your score by dozens of points. You’re entitled to a free copy of your report annually from each major bureau at AnnualCreditReport.com.

If you notice inaccuracies, dispute them immediately. The bureaus must investigate and respond within 30 days. Fixing one reporting error could be enough to raise your score significantly before you apply for a mortgage.

Key takeaway: Every choice you make with credit—how much you spend, when you pay, and what you open—directly shapes your path toward a better mortgage offer.

Quick Wins: Steps You Can Take This Month to Raise Your Score

Even with a short timeline, you can still make meaningful improvements in a matter of weeks. Think of this phase as a quick tune-up before your big financial moment.

Immediate actions that deliver fast results:

- Review your reports for errors. Start at AnnualCreditReport.com and check all three bureaus—Experian, Equifax, and TransUnion. Correcting an error can add points fast.

- Pay down credit card balances. Reducing utilization below 30% (ideally 10%) has one of the biggest and quickest impacts.

- Ask for higher credit limits. Increasing your available credit while keeping spending steady instantly improves your utilization ratio.

- Set up autopay. Even one late payment can stay on your report for seven years.

- Become an authorized user. Your score might be raised by a family member or acquaintance who has good credit and low balances.

If you can’t pay down everything at once, focus on the cards with the highest utilization or the highest interest rates. Lenders often view those balances as riskier.

Within 30 to 60 days, you might start seeing results from these steps. Even a 20–40 point boost can move you into a better rate bracket, saving thousands over time.

Key takeaway: You don’t need a year to improve your credit—focus on smart, high-impact moves that show progress fast.

Smart Habits to Build Long-Term Credit Strength

Building and keeping a high credit score isn’t about luck—it’s about developing strong, consistent financial habits that show lenders you can be trusted. Once you’ve improved your score, maintaining it is what truly makes the difference when you’re preparing for major financial milestones like buying a home.

1. Keep Your Oldest Accounts Open

The length of your credit history plays a significant role in your credit score. Many people close old credit cards after paying them off, thinking it simplifies their finances. But in reality, it can shorten your credit history and lower your average account age—both of which can hurt your score.

Best practice:

- Keep old accounts active by making small purchases (like subscriptions).

- Pay off those balances in full every month.

- Avoid unnecessary account closures unless there’s an annual fee you can’t justify.

2. Pay Every Bill on Time

Payment history makes up 35% of your credit score—the largest single factor. Your score can be negatively impacted for months and remain on your report for years if you miss even one payment.

Smart tips:

- Set up automatic payments for all credit cards and loans.

- Use phone reminders or budgeting apps to track due dates.

- If you’re struggling, contact creditors early to arrange alternate payment plans.

3. Keep Credit Utilization Low

Your credit usage ratio shows the percentage of your available credit you are using. It’s the second most important factor after payment history.

| Credit Utilization Level | Impact on Credit Score |

| Under 10% | Excellent – shows very responsible credit use. |

| 10%–30% | Good – still safe and favorable to lenders |

| 30%–50% | Fair—can start to raise red flags. |

| Above 50% | Risky – may lower your score significantly. |

Quick actions:

- Pay balances before billing cycles close.

- Request higher credit limits from existing lenders.

- Distribute purchases across different cards to avoid high single-card usage.

4. Diversify Your Credit Mix

A healthy mix of credit—like a credit card, personal loan, or auto loan—shows you can manage various financial responsibilities. Don’t rush into taking new credit just for variety, but if you’re building credit, a small installment loan can add positive diversity to your profile.

5. Monitor Your Reports Regularly

Keeping an eye on your reports helps catch potential errors or fraudulent activity early. Use tools like or to monitor your credit for free.

What to watch for:

- Unexpected hard inquiries

- Accounts you don’t recognize

- Incorrect payment statuses or balance errors

Strong credit habits are like good daily routines—they build stability, trust, and peace of mind over time. When you maintain these habits, you’ll not only protect your score but also create the kind of financial reliability that lenders and future opportunities reward.

Key takeaway: Long-term credit strength grows from small, steady actions. Paying on time, keeping balances low, and maintaining old accounts build the foundation for lifelong financial confidence.

Timing It Right: How to Plan Your Home Purchase Around Your Credit Goals

Timing can make or break your mortgage application. Improving your credit score is one thing—but ensuring that improvement aligns with your home-buying timeline is what gives your effort real payoff.

1. Start Planning at Least 6–12 Months Ahead

Your credit score changes gradually, not instantly. Begin improving your credit about a year before you apply for a mortgage. That gives enough time for updates—such as lower balances or corrected errors—to be reflected in your report.

Why timing matters:

- Credit bureaus update data monthly, not immediately.

- Inquiries and account changes need time to stabilize.

- Lenders prefer steady financial patterns rather than sudden spikes.

2. Follow a Step-by-Step Credit Timeline

Here’s a practical roadmap to follow as you prepare:

| Months Before Buying | Action Step |

| 12 Months | Check all three credit reports and dispute any errors. |

| 9 Months | Focus on reducing card balances below 30% utilization. |

| 6 Months | Don’t apply for new loans or credit cards. |

| 3 Months | Continue on-time payments and keep accounts in good standing. |

| 1 Month | Get preapproved for your mortgage and review your score again. |

By following this plan, you give your score time to improve naturally while building a positive pattern that lenders can see.

3. Manage Your Debt-to-Income Ratio (DTI)

Lenders look beyond credit scores—they also measure how much of your income goes toward debt. A DTI below 36% is generally ideal, showing you have room in your budget for a mortgage.

How to improve DTI:

- Pay off high-interest debts first.

- Avoid financing new large purchases.

- Consider side income or bonuses to increase earnings.

4. Avoid Major Financial Changes

Lenders may become concerned if you open new credit accounts, make large purchases, or change employment just before applying for a mortgage. They prefer consistency—steady income, predictable spending, and no sudden financial shifts.

5. Review and Lock In Your Score

About a month before applying, pull your reports again and check for updates. If everything looks strong—low balances, no errors, and a solid payment record—it’s time to move forward with preapproval.

With the right timing and a steady approach, you’ll walk into your mortgage application with confidence, knowing your credit score tells a story of reliability and control.

Key takeaway: Good timing turns preparation into power. By improving your credit steadily and planning, you’ll secure better rates, lower payments, and a smoother path to homeownership.

Conclusion

Your credit score is a representation of your financial behavior, not just a number. By understanding what impacts your score and taking steps early, you’ll position yourself for better mortgage rates and long-term financial confidence. The work you do now could mean saving thousands later.

Prior to purchasing a home, raising your credit score requires planning, consistency, and timing rather than perfection.

Frequently Asked Questions

How long does it take to improve a credit score?

It depends on your starting point, but most people notice progress within one to three months after paying down debt or correcting errors.

Does checking my credit hurt my score?

No. Your credit score is unaffected by checking your own credit, which is regarded as a soft inquiry.

Should I close old credit cards before applying for a mortgage?

No. Closing old accounts can shorten your credit history and hurt your score.

What’s the minimum score to buy a house?

For most FHA loans, a 580 score is the minimum, but aiming for 620 or higher opens better loan options.

How often should I check my credit report?

At least three times a year—once from each credit bureau—to make sure your information is accurate.

Additional Resources

- – Learn how credit scores impact mortgages.

- – Explore how your credit affects loan options.

How to Get Pre-Approved for a Mortgage Fast

<?xml encoding=”UTF-8″>

Buying a home is exciting, but waiting for pre-approval can feel like forever—especially when the market is moving fast. The quicker you get pre-approved, the sooner you can shop confidently, make stronger offers, and move closer to owning your dream home. This guide breaks down how to speed up the process while staying organized and stress-free.

Why Getting Pre-Approved Fast Matters More Than You Think

Speed in pre-approval isn’t only about convenience—it’s about leverage. In today’s housing market, sellers are flooded with offers, and many won’t even consider bids from buyers who aren’t pre-approved. That single document signals that your finances have already been vetted and you’re ready to act. It’s a credibility badge that can move your offer to the top of the pile.

Beyond competition, pre-approval gives you a financial roadmap. It outlines your borrowing limit, expected payments, and loan types that fit your situation. Knowing these details early helps you avoid wasting emotional energy on homes outside your range or scrambling to adjust your expectations later.

A fast pre-approval process is possible when you remove the common obstacles—missing documents, slow communication, or credit issues. Many buyers lose time because they underestimate how detailed lenders need to be. The process isn’t just about your income; it’s also about consistency, debt levels, and how responsibly you’ve managed money over time.

How quicklycan pre-approval benefit you?

- Stronger offers: Sellers favor buyers with verified funding.

- Faster closings: Pre-approved buyers already have much of the work done.

- Less stress: Before you fall in love with a house, you know exactly how much you can afford.

- Negotiation power: Real estate agents treat pre-approved clients as priority prospects.

When your lender already has all the required details upfront, they can often issue a pre-approval within 24 to 48 hours. However, if they have to keep chasing paperwork, that timeline stretches into a week or longer. Your readiness directly impacts your speed.

Key takeaway: Fast pre-approval isn’t luck—it’s the result of preparation and proactive communication. The more ready and responsive you are, the sooner your lender can say “yes.”

The Documents You Need to Gather Before You Apply

If pre-approval is a race, documentation is your fuel. Lenders need to verify who you are, how much you earn, and how responsibly you handle finances. When you provide all of this in one clean package, your lender can review and approve your application quickly—sometimes within a single business day.

Here’s what you’ll need to have ready:

| Category | Examples | Purpose |

| Income Proof | W-2s, recent pay stubs, tax returns (last two years) | Verifies consistent income and stability |

| Credit Records | Credit report, list of outstanding debts | Confirms payment history and debt-to-income ratio |

| Assets | Bank statements, investment, or retirement accounts | Proves available funds for down payment and closing |

| Employment Verification | Employer contact, offer letter if new job | Ensures steady employment history |

| Identification | Driver’s license, Social Security card | Confirms legal identity and citizenship status |

If you’re self-employed, lenders will also need your business tax returns, 1099 forms, and a year-to-date profit-and-loss statement. Because your income fluctuates, they’ll want to see at least two years of consistent revenue.

Tips to stay organized:

- Create a digital folder containing all documents, clearly labeled.

- Use PDF versions for easy upload to your lender’s portal.

- Double-check expiration dates on identification.

- Include explanations for any income gaps or irregular deposits.

Some lenders offer automated verification tools that can pull your tax or payroll data directly from trusted sources, such as the IRS or payroll systems. Opting for these can shorten your wait time even more.

Key takeaway: Document organization is the single most powerful way to accelerate pre-approval. The more complete your submission, the fewer delays you’ll face.

How to Immediately Raise Your Credit Score Prior to Pre-Approval

Credit plays a starring role in how lenders see you. Faster acceptance, cheaper loan rates, and easier underwriting can result from even a slight increase in your credit score. The good news? You can improve your score in a couple of weeks; it doesn’t have to take months.

Here’s how to move the needle fast:

- Pay down high balances: Keeping your credit utilization below 30 percent boosts your score quickly.

- Check for reporting errors: Visit AnnualCreditReport.com to review your credit reports. If you find mistakes, dispute them immediately with the credit bureau.

- Make all payments on time: Even one late payment can cause delays or higher rates.

- Avoid new credit applications: Each inquiry temporarily lowers your score.

- Keep old accounts open: Your credit history length helps your score, so avoid closing older cards.

If your score is below 620, many lenders will still work with you, but you’ll need to show stability in other areas—like consistent income or larger savings reserves. You can also explore government-backed loans such as FHA or VA programs, which often allow lower scores.

Quick-impact actions table

| Action | Potential Impact | Time to See Results |

| Paying down credit cards | Increases the utilization ratio | 1–2 weeks |

| Correcting credit report errors | Removes false negatives | 2–4 weeks |

| Setting up auto-pay | Prevents missed payments | Immediate |

| Avoiding new inquiries | Stabilizes score | Ongoing |

Improving your credit doesn’t just make approval faster—it helps you qualify for better loan terms. Even a 20-point increase can save thousands over the life of your mortgage.

Key takeaway: A clean, strong credit profile speeds up approval and strengthens your negotiating power. Start improving it before you apply.

Choosing the Right Lender for Speed and Reliability